Modern Portfolio Theory

We believe in a “Bottom Up” approach believing there are only a handful of managers out of thousands who, over the long-term, have done better than the market. We see evidence of that in looking at the track records of such investment gurus as Warren Buffett, Rowe Price, Ken Fischer, Sr., and John Templeton, each of whom was able to achieve an average annualized return of over 20% for 25 years (returns that are considerably more than market returns, according to “The Money Managers”, by John Train, 1985).

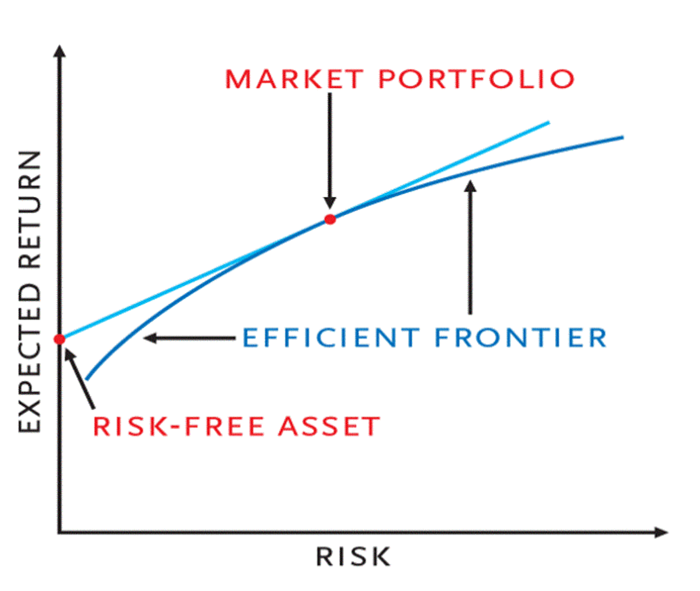

The “Top Down” (Modern Portfolio Theory) approach was begun when Harry Max Markowitz wanted to quantify stock price movements. He theorized that stock price fluctuations were due to two influences. The first was the overall stock market. When the stock market is moving up, there is a tendency for all stocks to move up; and conversely, when the stock market moves down, all stocks tend to move down. Markowitz termed this portion of the volatility “beta risk.” Markowitz further defined company specific risk, or “alpha,” as the volatility due to the impact of company specific volatility. Markowitz went further to define what he termed “The Efficient Frontier” and theorized there existed a relationship between return and risk where the higher return was associated with higher risk. Removing the beta portion of volatility would leave a curve defining the Efficient Frontier.

In 1986 Brinson, Hood, and Beebower (BHB) published a study about asset allocation of 91 large pension funds measured from 1973 to 1985. Their findings showed the great majority of risk (volatility) was due to the beta factor. Subsequent studies of mutual funds and pension funds confirmed this study and depending on the source, generally accepted by Top Down adherents is that between 85% to over 90% of the risk (volatility) is due to alpha risk and little is due to the beta or company specific risk. The Top Down approach to investing, then, begins with looking at the economy and making forecasts of which industry will have the best returns and then looks at the specific companies within that industry.

The Top Down approach tends to seek a diverse portfolio spread across industries.

On the other hand, the Bottom Up approach to investing overlooks economic conditions and focuses on selecting stocks of companies which have favorable attributes. This approach assumes that companies can do well even when their industry is not doing well. It entails a thorough review of the company: its financials, its products, its competitive position, its management. In 1997 William Jahnke challenged the results of the Brinson, Hood, and Beebower study. Jahnke using the same data found the 10 year annual returns of the benchmarks for the 91 pension portfolios ranged from 9.47 percent to 10.57 percent (a spread of 1.1 percent). The actual returns of 91 pension portfolios were 5.85 percent to 13.4 percent a spread of 7.55 percent). Based on this, the expected range of 1.1 percent divided by the actual range of 7.55 percent means that asset allocation explained just 14.6 percent of portfolio performance. The phrase “Don’t put all your eggs in one basket” is a strategy of diversification and part of the Top Down Modern Portfolio Theory approach to investing.

Warren Buffett, perhaps the greatest investor of our time prefers the other approach (Bottom Up) saying, “Put all your eggs in one basket and watch the basket.” (The Snowball: Warren Buffett and the Business of Life, 2008)